Investment Philosophy

The Investment Philosophy that Nicolette Financial adheres to are the (4) tenets of Modern Portfolio Theory (MPT):

(1) Markets Are Inherently Efficient

Markets process all available information so rapidly in determining the price of any security that it is statistically improbable to gain a competitive edge by exploiting the occasional anomalies. This means that to “beat the market”, an investor would have to possess not only the correct insight or information regarding a specific security, he would have to be the only investor to possess it, and he would have to do this consistently over time.

(2) Exposure to Risk Factors Determines Investment Returns

Academic studies have confirmed that an investor’s return is overwhelmingly dependent on exposure to the specific risks associated with the various asset classes. Over time, riskier assets provide higher expected returns as compensation to investors for accepting the greater risk. This is the basic concept underlying the Nobel prize-winning strategy that has become the new legal standard for prudent investing by fiduciaries.

(3) Diversification Reduces Portfolio Risk & Increases Expected Returns

Adding low-correlating asset classes, even if they carry a higher risk on their own, can actually reduce overall volatility on a portfolio level, and increase expected rates of return. By intentionally designing portfolios to incorporate various degrees of exposure to different asset classes, we can help investors to create the most efficient (highest expected return) portfolio for the level of risk they are willing to assume.

(4) Disciplined Portfolio Management Increases Expected Returns

The traditional way of managing investments—active stock picking—has been based on forecasting growth and earning in attempts to “beat the market”. This strategy is expensive in terms of trading costs and tax liabilities passed along to the individual investor. Instead, Nicolette Financial will add value through a disciplined approach starting with the assumption that markets are extremely competitive and profiting from anomalies is improbable.

Many investors understand the importance of maintaining asset allocation targets by periodically rebalancing a portfolio. In advocating for a rules-based approach, we would emphasize employing a method of rebalancing that attempts to enhance portfolio growth over time, rather than the most common type of automatic rebalancing, which is purely calendar-driven.

A Fiduciary Standard

A Fiduciary Standard means that your financial advisor is putting your interests first.

Under the Prudent Man Rule, when the governing trust instrument or state law is silent concerning the types of investments permitted, your fiduciary is required to invest trust assets as a “prudent man” would invest his own property, keeping in mind the needs of the beneficiaries, the need to preserve the estate (or corpus of the trust), and the amount and regularity of income.

The Prudent Man Rule is based on common law, stemming from the 1830 Massachusetts court decision — Harvard College v. Armory, 9 Pick. (26 Mass.)446, 461 (1830). The Prudent Man Rule directs trustees

“to observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.”

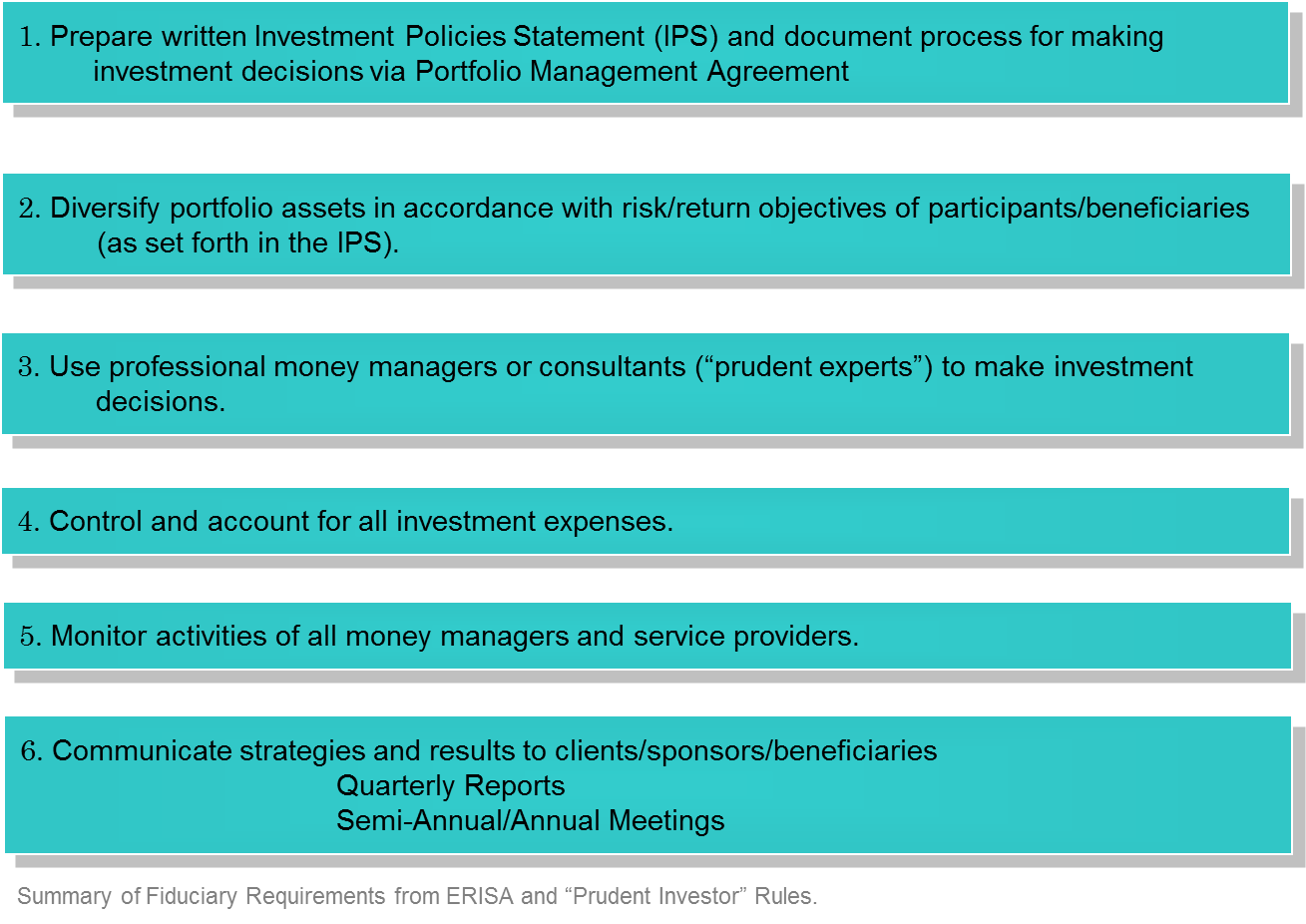

Summary of Fiduciary Requirements from ERISA and “Prudent Investor” Rules